Everyone can create money

Download the WEA commentaries issue ›

“Everyone can create money; the problem is to get it accepted“

Hyman Minsky

Summary. Central banks the world over publish sophisticated Flow of Funds data which shows who and how and, to an extent, why all kinds of money are created and used and if stocks and flows of debt and money are becoming a threat to stability. Institutional analysis of these data, which looks at different kinds of credit as well as at different kinds of money and using a grid which enables the economist to distinguish between different kinds of economic sectors shows that they can be used to gauge the (in)stability of an economy. Macro-economists have too often however only looked at crude aggregates of total money or even purged money from their models while analysis of credit is, in 2017, still wanting as the connection between all kinds of money and all kinds of credit is still absent from the models, even if a monetary sector is increasingly added to these models.

This piece benefitted from helpful remarks by Josh Mason and Diane Coyle.

- Introduction: the measurement of monies

Money is measured by statisticians working at central banks. Or rather, some kinds of money are recorded by these statisticians. Others aren’t. Stamps can be a work of art (picture 1, super model Doutzen Kroes photographed by super photographer Anton ‘Joshua tree’ Corbijn).1

But stamps are not only tokens of art. They are money, too. Even when we use the restricted functional definition of money which can be found in most textbooks, which defines money as a store of value, a means of exchange and a unit of account, it is clear that stamps are money – including, nowadays, their own unit of account. But the question why it’s a means of exchange etc. is of course more interesting: we trust ‘the post’ to deliver our letters (dwindling market) and packages (increasing market). And to honor this implicit contract. And rightly so. Dutch stamps have for some years been their own unit of account but I can still use my Euro dominated ones which occasionally surface from the occasional drawer.

Stamps are not the only kind of private, market based money (though I have to add that property rights and contracts are designed and guaranteed by the government). Commercial credits are another and quantitatively much more important kind. The balance sheet of Shell alone listed, for the first quarter of 2017, ‘trade and other receivables’ of $44 billion and ‘trade and other payables’ of $49 billion, which were listed as ‘current assets’ and which shows that these receivables and debts are a store of value, in this case recalculated in dollars. And I have to stress this: when a buyer emits a receivable, i.e. a promise to pay, this results in a legal sale, guaranteed by the government. Rights of ownership are transferred. The buyer can, if he or she wants, resell the oil or the book or the skirt or whatever. And often, the resulting ‘receivables’ can be traded on some kind of market. They do have a degree of liquidity.

Morris Copeland, the institutional economist who designed the widely used Flow of Funds statistics

- The measurement of money

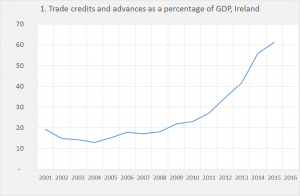

Emitting receivables is a way to enable monetary economic exchange. Like stamps, these debts are not recorded by central bank statisticians. But they are recorded by national accounts statisticians, as part of the flow of funds data as well as balance sheet data. The USA Flow of Funds were developed by the institutional economist Morris Copeland, who should have been awarded a Nobel prize for this.2 At this moment, all mayor central banks estimate and publish these data; the USA Flow of Funds lists the payables and receivables as ‘trade payables’ and ‘trade receivables’ and treats them as a means of payment. Graph 1 shows the most remarkable recent development of ‘payables’ of the Europe Flow of Funds data, estimated by the ECB but in this case published by Eurostat.

This is not the place to use these data to analyse economic development but they are fully consistent with the idea that the transfer of ‘intangible assets’ by companies like Microsoft from the USA to Ireland has been financed by intercompany ‘receivables’ and ‘payables’ – an ‘inter-company debt’ financed transfer of property rights, which reminds us of the Minsky quote above this article. Payables and receivables are however mostly used to finance transactions (selling and buying) between companies and are therewith indispensable for the functioning of a monetary economy: private, market based money. And stocks and flows of this kind of money are estimated by national accounts statisticians.

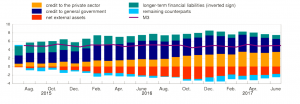

As stated, central bank statisticians estimate money, too, and this time of the more normal kind. It is worthwhile to go a little deeper into this, using the monthly ECB ‘monetary developments’ press release (June 2017 in this case).

Graph 2. Contribution of the M3-money counterparts to the annual growth rate of M3

This monthly press statement is not just consistent with but an excerpt from the Flow of Funds, highlighting the flows which influence the change of M3 money, the definition of money preferred by the ECB which defines money as coins, notes and deposit money, albeit only short term deposits. The Flow of Funds character shows by the ‘counterparts’, surprising to some may be the fact that during the last two years bank lending to the government dominated money creation in the Eurozone. Just as it did in the thirties in the USA – a fact which according to Koo is not acknowledged by Friedman and Schwartz in their ‘A history of money in the USA, 1867-1960’.

There is more to this: we can ask the question why it is possible for private banks to issue legal tender in the first place. The answer is that they do not do this. Banks issue ‘deposit money’, not legal tender. As is well known, deposit money is issued by a large number of banks (not all of them, they do need government approval to be able to do this). And here comes the trick: the government, aka the central bank, guarantees a 1:1 exchange rate between notes, coins and deposit money – no matter which banks issued it. And the government (aka central and local government) also accepts all deposit money, no matter which bank issued it, as a means to extinguish private tax debts. Which means that all deposit money has a 1:1 exchange rate, no matter which bank issued it (in the Eurozone this went off track in Greece and Cyprus). Returning to the graph: this is all about deposit money issued by banks to counterparts, like households (mainly mortgages), non-financial companies (loans and short term commercial credit) and the government. Mind that while central banks are not allowed to finance the government by printing money (at least not in the Eurozone), private banks are allowed to do so. The ‘longer-term financial liabilities’ are deposit money which flows from long term deposits into short-term deposits and therewith into M3 money; net external assets is the net amount of Euros stacked away in the Bahamas or used to buy Chinese stocks. Clearly, central banks use a credit based idea of money and do not only look, like Milton Friedman did, at the total amount of money but also, using flow-of-fund statistics, at the relation between money and credit. Again, then the graph comes straight from the monthly press release of the ECB and in fact follows a Bundesbank tradition which dates back at least to the beginning of the seventies. Summarizing: economists have developed detailed, dependable systems to measure flows and stocks of all kinds of money which are used in all major central banks and which enable analysis of monetary developments and economic risk.

- Money in the models

Given the centrality of Flow of Funds statistics to the working of central banks, the extent to which, surely before 2008, money was removed from mainstream macro is puzzling. There is no need to dwell on this. Charles Goodhart in November 2007 with his ‘Whatever became of the monetary aggregates’ and Willem Buiter in March 2009 with his ‘The unfortunate uselessness of most ‘state of the art’ academic monetary economics’ have ridiculed, lambasted and vilified this approach to money. As Buiter remarks about monetary economics which does not have ‘money’ as one of the variables in its models and which does not model a financial sector: “Both the New Classical and New Keynesian complete markets macroeconomic theories not only did not allow questions about insolvency and illiquidity to be answered. They did not allow such questions to be asked.” To state this in a more practical way we can quote Peter Bofinger and Mathias Ries, who very recently (while I was writing this, in fact) published a Voxeu post on this topic and show how introducing money into the models enables questions and answers (emphasis added):

“In the case of China, the causal chain of the monetary analysis is diametrically opposed to the logic of the real analysis. In the real analysis, high Chinese saving has been created independently of developments in the US. In the monetary analysis, Chinese saving, above all profits from the corporate sector, were generated as a result of US consumers buying more and more Chinese products. The propensity to consume in the US was fueled by the reduction in the US saving rate due to the housing boom and by the very low interest rates offered by the Federal Reserve.

The monetary analysis logic also makes it possible to overcome the ‘paradox of capital’ (Prasad et al. 2007). The real analysis cannot explain why capital, which is assumed to consist of the standard commodity, should flow from China to the US, where the returns of capital are supposed to be lower. In the monetary analysis, capital flows consist of money and it is not paradoxical that US-dollar payments made for consumption goods from China were recycled by the Chinese central bank into the US capital market”.

The question is whether this has improved. The short answer is: it seems that way. Newer models, published by the ECB in June 2016, do bear titles like “EAGLE-FLI. A macroeconomic model of banking and financial interdependence”. However… looking at footnote 4 from this study we encounter the next phrase: “In line with these contributions, we assume a cashless economy, so there is no explicit role for money”. Of course, ‘these contributions’ are earlier studies, six in total of which five date from after 2008. Even if money plays a role in such model, it is also not the credit kind of money which is estimated in the Flow of Funds but a ‘loanable funds’ kind of money, an exogenous asset with a restricted supply which enables people to lower transaction costs of exchange but which is not based upon social trust or bonds or market transactions, like the mortgages of the monetary statistics, like stamps or like commercial credits. Or like the short term commercial credits which initially financed the up to 15% of GDP current account deficits of the GIPSI nations. Or the ‘wall of money’ which was created by the mortgage boom mentioned above, stacked away in savings accounts and which, in countries like the Netherlands, at this moment drives up house prices as children are borrowing this money from their parents.

It’s all a bit disheartening. Fortunately, Flow of Funds analysis based upon accounting models instead of calculus and discounting based models is having a boost. Bofinger and Ries, who explicitly discuss the difference between Flow of Funds analysis and mainstream modelling, have already been mentioned. And the ECB publication, ‘Flow of funds analysis at the ECB. Framework and applications’ states:

“Euro area financial account data have been published at an annual frequency since 2002 and at a quarterly frequency since 2007 (partial data were first published as early as 2001). Flow-of-funds analysis at the European Central Bank (ECB) has developed based on this expanding set of data, in addition to available country data, in support of the ECB’s economic and monetary analysis.”

Also, the recent work by Josh Mason, Arjun Jayadev and Amanda Page-Hoongrajok, ‘The Evolution of State-Local Balance Sheets in the US, 1953-2013’, reminds us of the classical 1962 article of Morris Copeland, ‘Some illustrative analytical uses of Flow of Funds data’ in which he states: “Section III offers a capital outlay function for state and local governments in which the independent variables are the current surplus of state and local governments and the ratio of federal national defense expenditures to total GNP.”

The availability of Flow of Funds data for the Eurozone means that ‘prophetic’ analyses based upon Flow of funds Analysis like ‘seven unsustainable processes’ by Wynne Godley can, by now, be pursued for the Eurozone, too (here an article which rightly describes Godley as the ‘Keynes of Flow of Funds, mind, again, that Flow of Funds analysis is by now part and parcel of the analyses of central banks) To get the gist of this kind of analysis: since 2008, the Eurozone current account changed from a deficit of around 2% of nominal GDP to a surplus of 3%. This means that economic performance of the Eurozone has been dismal (in a historical as well as a comparative perspective) despite this 5% of GDP boost to spending. Or, a boost to spending? In fact, the change was, to considerable extent, caused by lower oil prices and though these might have caused higher consumption of oil related products, such an increase will of course not have changed a current account deficit into a current account surplus. The shift simply means that more money is staying inside the Eurozone – looking at this from the monetary side it shows that a price decrease for oil leading to a more favorable current account does not directly boost domestic activity. Which means that domestic spending will have to do the job which, considering high levels of household as well as government debt (which, in the Eurozone, is designed to be a binding constraint) this will either have to be financed by profits (investment) or higher total wages (household consumption). Or a higher level of trade credits and bank lending… It is important to note that it is not the wage level and surely not real wages which are important here, but total nominal wages.

The kind of DSGE (Dynamic Stochastic General Equilibrium) models linked to above, which still have no role for money and look at capital and imports and exports as ‘goods’ are of course not the only macro models. Other strands of models did take money and the monetary aggregates more seriously. One can think of the work of Milton Friedman who paid attention to money growth. But he did not look at credit and used a fairly restricted definition of money, therewith disregarding the Flow of Funds data. Against this background, his concepts look crude and clumsy while this strain of thinking tended to rule out destabilizing effects of credit, loans and borrowing, as also shown in ‘The Age of Turbulence’, the autobiography of Alan Greenspan who, in 2007, explicitly stated that debt, national or international, won’t ever be a problem as markets and people optimize (to his defense, ‘This time is different. Eight centuries of financial folly’ by Carmen Reinhart and Kenneth Rogoff was only published in 2009. Clearly, the turbulent age of Greenspan was not that different).

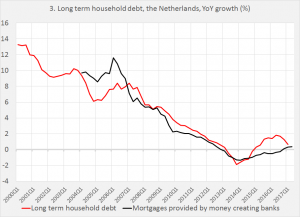

A more sophisticated way of thinking was the Bundesbank tradition, which was adopted by ECB. It does take credit seriously and even tends to see 5% M3 money growth as ‘stable’ because it shows a healthy growth of credit. It also distinguishes different sectors when it comes to borrowing, therewith implicitly also looking at the ‘counterparts’ of money creation. The names of people like Otmar Issing, the first senior economist of the ECB, are connected to this. Rereading Issing and checking the 1974 yearly report of the Bundesbank, which he cites as a watershed, reveals that Issing misrepresents history. The post 1929 deflation was much more damaging to Germany that the 1923 inflation, though Issing rightly also mentions the (much, much less severe) 1946/1947 inflation. I however dare to say that, in 1945-1947, relatively mild inflation was not the largest problem in Germany. He also overstates the independence of the Bundesbank (p. 26 of the 1974 report states that the Bundesbank lends to the German government – which is a total taboo for the ECB). It is however remarkable that the 1974 yearly report shies away from a genuine analysis of stocks and flows of credit and instead retverts to the Friedman style of thinking, which basically only looks the amount of what boils down to a restricted definition if money. Flow of Funds and stock data are richly available in the report, but attention is suddenly focused on flows of M3 money. As increases in M3 money may have different origins – in one period bank lending to the government may dominate, in another period lending to non-financial companies or mortgage lending to households – this is a too restricted way too analyze monetary developments. The Bundesbank approach surely was more subtle and flexible than the technocratic approach of Friedman style monetarists. Also, surely there below the surface an analysis of sectoral flows of credit can be witnessed. But it was still blunt and crude when compared with the subtle analysis possible by using Flow of Funds data which show supply as well as use of money and credit. All in all it is remarkable that, though central banks do publish and use sophisticated macro-economic Flow of Funds data, macro-economic theorists – also those at central banks – have shied away from this model. To show, again, the possibilities of such data to illustrate and analyse total long term debt of households as well as total mortgage credit provided by ‘Monetary Financial Institutions’, or money-creating banks. As can be seen, both series are quite close to each other, differences can be explained by the fact that households also borrow from pension funds and comparable non-money creating financial institutions. Which is interesting. We do have the information which shows how rapidly debts increased during the years of what is called the ‘Great Moderation’ while, in the Netherlands, post 2008 no meaningful deleveraging took place. But an even more remarkable aspect of these data is that before 2008, house price increases were fueled by increases in mortgage lending. At the moment of writing of this piece, house prices as well as the number of real estate transactions are on the rise again in the Netherlands. With an increase of 8%, house prices are rising way faster than the consumer price level or wages. But this time is different: these increases are not fueled by reckless lending by large banks. It’s up to the economists to find out what’s different, but the Flow of Funds data enable us to ask the question.

Turning to the Eurozone: before 2008, comparable data were available and assembled at the ECB (even though monetary statisticians in for instance the Netherlands neglected to map securitized mortgages…). Alas, the ECB focused totally on a limited definition of inflation data, disregarded its own information and turned blind eye to rapidly increasing private debts (+30% in some years in Ireland…). While people like Morris Copeland and Wynne Godley had shown how to use data on flows and stocks of money, income and debt. We do have the data. Now, economists have to start to use them. To end with a quote by Morris Copeland (h/t V. Ramanan):

“The subject of money, credit and moneyflows is a highly technical one, but it is also one that has a wide popular appeal. For centuries it has attracted quacks as well as serious students, and there has too often been difficulty in distinguishing a widely held popular belief from a completely formulated and tested scientific hypothesis.

Source: Centraal Bureau voor de Statistiek; De Nederlandsche Bank

I have said that the subject of money and moneyflows lends itself to a social accounting approach. Let me go one step farther. I am convinced that only with such an approach will economists be able to rid this subject of the quackery and misconceptions that have hitherto been prevalent in it.

Reference

Copeland M A, “Social Accounting For Moneyflows”, Chapter 1 of Dawson J C (1996) Flow-of-Funds Analysis: A Handbook for Practitioners, New York: M E Sharp [article originally published in 1949]

______________________

1 A super model instead of a dead president on money is of course ‘Zeitgeist’. The increased prominence of super models is a sign of a more feminine culture.

2 Speaking of this, if we accept that Robert Solow and Milton Friedman would not have been able to co-author their mayor works on money and growth without Anna Schwartz, she also missed out on one. Even she seems however not to have been able to grasp the interconnectedness of money and credit spelled out in the Flow of Funds.

From: pp.2-5 of WEA Commentaries 7(4), August 2017

http://www.worldeconomicsassociation.org/files/Issue7-4.pdf

The money which we can create by writing checks is a kind of money which has a time limit till when the newly created money is debited to ones checking account. Thus there are two kinds of money and the other kind being currency has no time limit.